This can be a visitor publish from Chris at PortfolioAtlas (a software that maps 100+ cities to the portfolio measurement you’d must retire in each).

When you’ve been across the FIRE group for greater than every week, you recognize the drill…

Spend lower than you earn, make investments the distinction, and let your financial savings price do the heavy lifting.

Push your financial savings price from 40% to 50% and also you knock years off the timeline. Push it to 65% and also you’re performed earlier than most individuals have paid off their automobile.

I’ve spent a number of time gazing that math. However there’s one other lever that just about no person in the neighborhood really pulls. It’s not how a lot you save, it’s the place you intend to spend it.

The 4% rule says your FIRE quantity is simply your annual spending instances 25. We obsess over the “instances 25” half and the financial savings price that will get us there. However “annual spending” is dominated by one variable most individuals deal with as mounted – the price of residing wherever you occur to reside. Change town and you modify the goal (generally by an element of 4).

I wish to present you what that appears like with actual numbers, why I feel geography is essentially the most underrated risk-management software in early retirement, and what number of years it may shave off your timeline.

How does location change your FIRE quantity?

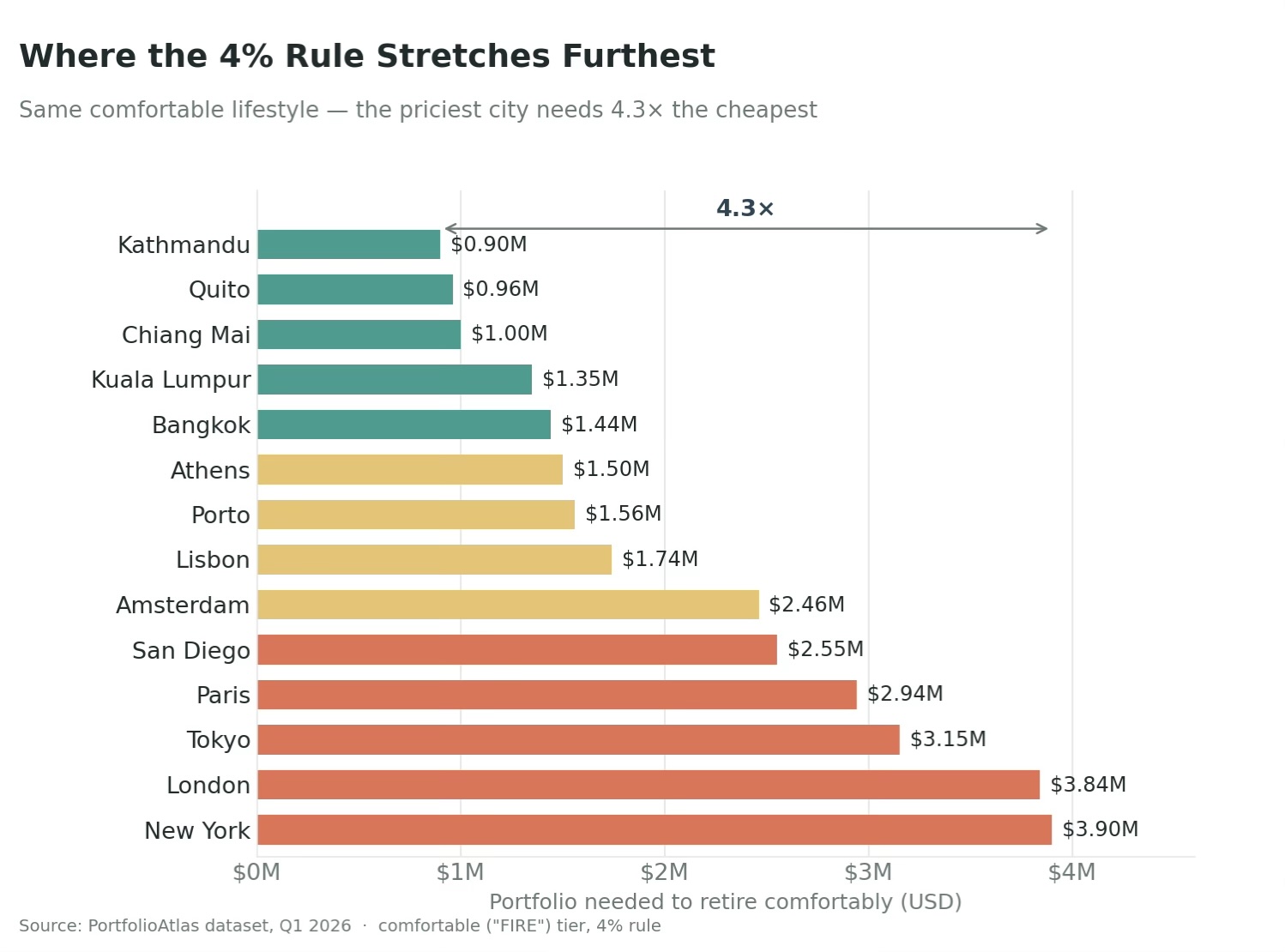

Right here’s the comparability that began all of this.

I took a single, mounted way of life (what I’d name a snug retirement) and held it fixed – a pleasant condominium, eating out often, respectable healthcare, the occasional journey. Then, I let solely town change and utilized the identical 4% rule to every.

The unfold is larger than most individuals guess:

| Metropolis | Snug FIRE Quantity | Month-to-month Spending it Helps |

|---|---|---|

| 🇳🇵 Kathmandu, Nepal | $900K | $3,000 |

| 🇹🇭 Chiang Mai, Thailand | $1.0M | $3,333 |

| 🇵🇹 Porto, Portugal | $1.56M | $5,200 |

| 🇺🇸 US common (46 cities) | $2.08M | $6,933 |

| 🇺🇸 San Diego, USA | $2.55M | $8,500 |

| 🇺🇸 New York, USA | $3.9M | $13,000 |

Identical way of life. The costliest metropolis within the dataset (New York, at $3.9M) requires 4.3 instances the portfolio of the most affordable (Kathmandu, at $900K). Put in another way: the hole between retiring in New York and retiring in Chiang Mai is roughly $2.9 million – greater than most individuals’s total FIRE quantity.

And this isn’t a narrative about slumming it. The $1M “snug” tier in Chiang Mai buys a personal pool villa or a premium apartment, common dinners at the perfect eating places on the town, a leased automobile, and premium worldwide medical insurance. It’s not deprivation. It’s only a completely different price ticket for the same life.

The patterns aren’t random, both. After I group the cities by area, they cluster the best way you’d count on:

- Southeast Asia (Chiang Mai $1M, Kuala Lumpur $1.35M, Bangkok $1.44M) and components of Latin America (Quito $960K, Medellín, the Mexican mid-tier $1.14M–$1.5M) anchor the low finish.

- Southern and Jap Europe sit within the snug center (Porto and Budapest round $1.56M, Athens and Valencia close to $1.5M–$1.56M).

- Western Europe and the worldwide monetary capitals run sizzling (Amsterdam $2.46M, Paris $2.94M, Tokyo and Hong Kong $3.15M, Singapore $3.24M, London $3.84M, New York $3.9M).

The takeaway is easy however beneath appreciated: your retirement quantity is generally a perform of geography, and geography is a alternative.

Most of us inherit it by default as an alternative of selecting it on objective.

Geographic arbitrage is a hedge

Right here’s the place it will get attention-grabbing, and the place I feel the FIRE group has been leaving one thing on the desk.

The scariest danger in early retirement isn’t a foul common return, it’s sequence-of-returns danger (i.e. a nasty market in your first few years, while you’re promoting belongings that received’t be capable of recuperate). The identical 30% drop does way more injury in yr one than in yr fifteen, since you’re drawing down a shrunken portfolio at precisely the unsuitable second.

The usual defenses are acquainted: a money cushion or bond tent, versatile withdrawal guidelines, a little bit of “Barista FI” earnings. All stable, however there’s one other lever that not often will get talked about, and the fee information makes it concrete: a versatile price base.

In case your spending can drop by relocating, your withdrawal price falls in exactly the years you most want it to.

Say you retire in San Diego with a snug $2.55M portfolio, drawing $102,000 a yr – a textbook 4% withdrawal. Then the market arms you a 30% drop in yr one. Your portfolio is now $1.785M, and that very same $102,000 is instantly a 5.7% withdrawal price – squarely within the hazard zone for a multi-decade retirement.

Now suppose you will have someplace to go. You progress to Porto, the place that very same snug way of life prices about $62,000 a yr:

| Response to the Crash | Annual Spending | Withdrawal Price on $1.785M |

|---|---|---|

| Keep in San Diego | $102,000 | 5.7% (dangerous) |

| Relocate to Porto | $62,400 | 3.5% (protected) |

| Relocate to Chiang Mai | $40,000 | 2.2% (very protected) |

You didn’t promote a single further share. You didn’t contact your asset allocation. You simply modified your burn price, and a harmful withdrawal price turned a conservative one, shopping for your portfolio years to recuperate.

The half I discover most compelling is that it is a actual possibility, within the monetary sense. It has worth even in case you by no means train it. You don’t must spend your retirement as an expat. You simply must be genuinely prepared and capable of transfer if the early years go badly.

Most hedges price you one thing on the best way in – money drag, decrease fairness publicity, a decrease withdrawal price endlessly. Retaining geographic flexibility is a hedge that doesn’t price you something up entrance.

Identical financial savings price, completely different end line

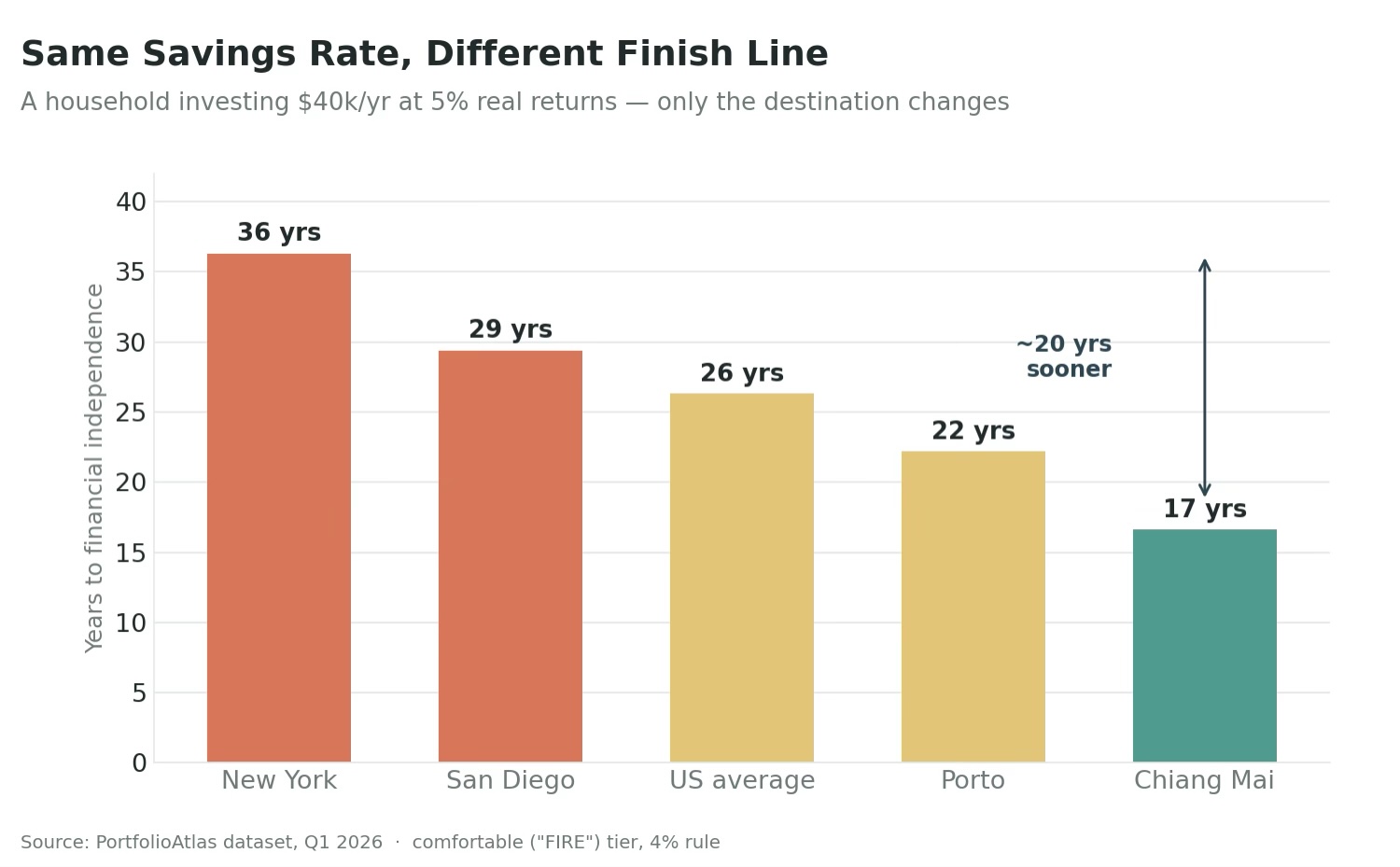

So if geography strikes the goal this a lot, what does it do to your timeline?

Let’s maintain the financial savings fixed and alter solely the vacation spot. Take a family investing $40,000 a yr, incomes a 5% actual return, ranging from zero. Right here’s how lengthy it takes to hit every FIRE quantity:

| Retire in… | FIRE Quantity | Years to get there | Years saved vs. New York |

|---|---|---|---|

| 🇺🇸 New York | $3.9M | 36.3 | – |

| 🇺🇸 US common | $2.08M | 26.3 | 10.0 |

| 🇵🇹 Porto | $1.56M | 22.2 | 14.1 |

| 🇹🇭 Chiang Mai | $1.0M | 16.6 | 19.7 |

Identical earnings. Identical financial savings. Identical returns. The one factor that modified is town you’re aiming at – and it’s the distinction between working one other 16 years or one other 36.

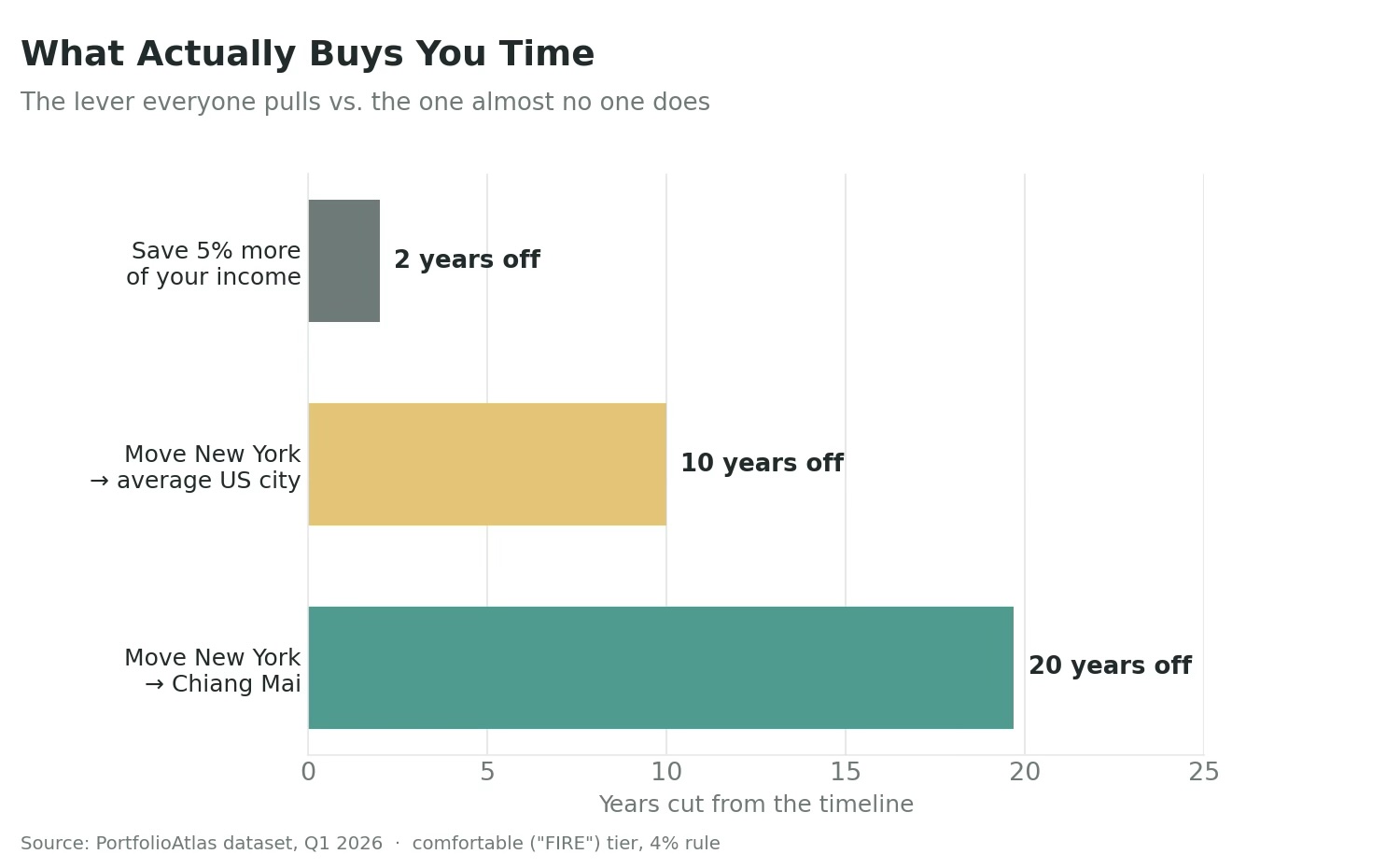

Now put that subsequent to the lever everybody really pulls. Our New York saver decides to get severe and bumps their financial savings price by 5 proportion factors – going from saving $40,000 to $45,000 a yr on a $100K earnings. Admirable. It cuts their timeline from 36.3 years to 34.3 years. Two years.

Selecting a mid-cost US metropolis as an alternative of New York? Ten years.

Selecting Chiang Mai? Almost twenty.

Bumping your financial savings price 5 factors buys you about 2 years. Altering your retirement vacation spot from New York to a median US metropolis buys you 10. To Chiang Mai, nearly 20.

That’s not an argument towards a excessive financial savings price. It’s an argument that we’ve been quietly ignoring a lever that’s typically a number of instances extra highly effective, simply because it lives on the spending facet of the equation and feels much less like a personal-finance choice and extra like a life choice.

Better of each worlds

There’s additionally a best-of-both-worlds model of this that’s price naming: you possibly can decouple the place you earn from the place you spend. Accumulate in a high-income metropolis, then retire someplace your cash goes additional. You get the fats paychecks throughout the climb and the low goal on the end. The geographic arbitrage doesn’t have to begin the day you cease working.

The trustworthy caveats

I’d be doing you a disservice if I made this sound like a free lunch, so right here’s the asterisk part.

- Healthcare – That is the massive one, particularly for US readers. A few of that low price of residing overseas assumes non-public insurance coverage in international locations the place care is great and low cost (Chiang Mai’s snug tier already budgets premium worldwide protection), however you have to plan it intentionally, and visa-dependent protection provides complexity.

- Visas and taxes – You don’t escape the IRS by shifting – US residents are taxed on worldwide earnings. Tax treaties, the International Earned Earnings Exclusion, and residency guidelines all matter, and so they’re price actual analysis (and an expert) earlier than you commit. This publish is technique, not tax recommendation.

- Foreign money and native inflation – A part of the arbitrage can evaporate if your house foreign money weakens or the native price of residing climbs sooner than yours would have at dwelling. A budget metropolis in the present day isn’t assured to remain low cost.

- The non-financial price – Household, mates, youngsters’ education, language, group – these don’t present up in a cost-of-living desk, and so they’re typically the actual deciding elements. The most affordable quantity shouldn’t be robotically the perfect life. Price is one enter, not the entire choice.

The purpose isn’t that everybody ought to transfer. It’s that everybody ought to value the choice. Geography is a lever sitting proper there on the dashboard, and most of us have by no means even touched it.

Find out how to run your personal numbers

If this reframed something for you, right here’s the three-step model:

- Pin down your actual way of life.

- Search for the FIRE quantity for 2 or three candidate cities at that way of life. We suggest you embrace your present metropolis because the baseline.

- Evaluate the timelines. Identical financial savings price, completely different end strains. The hole is commonly measured in years, not months.

That’s precisely what I constructed PortfolioAtlas to do. It maps a portfolio to each metropolis the place it’s sufficient, throughout 100+ cities and 47 international locations, with price breakdowns and Monte Carlo-simulated confidence ranges for each. You possibly can evaluate any cities facet by facet to see the timeline hole for your self (and since that is the Mad Fientist viewers: each quantity right here makes use of the 4% rule, however the software fashions longer-horizon withdrawal charges too, as a result of a 45-year retirement isn’t the identical animal as a 30-year one).

Financial savings price is the lever everybody pulls. Geography is the one nearly nobody does. And for lots of people, geography is the larger of the 2.

Chris runs PortfolioAtlas, a free software that exhibits you the place on the earth your portfolio can purchase you monetary freedom. All figures are from the PortfolioAtlas dataset, Q1 2026.