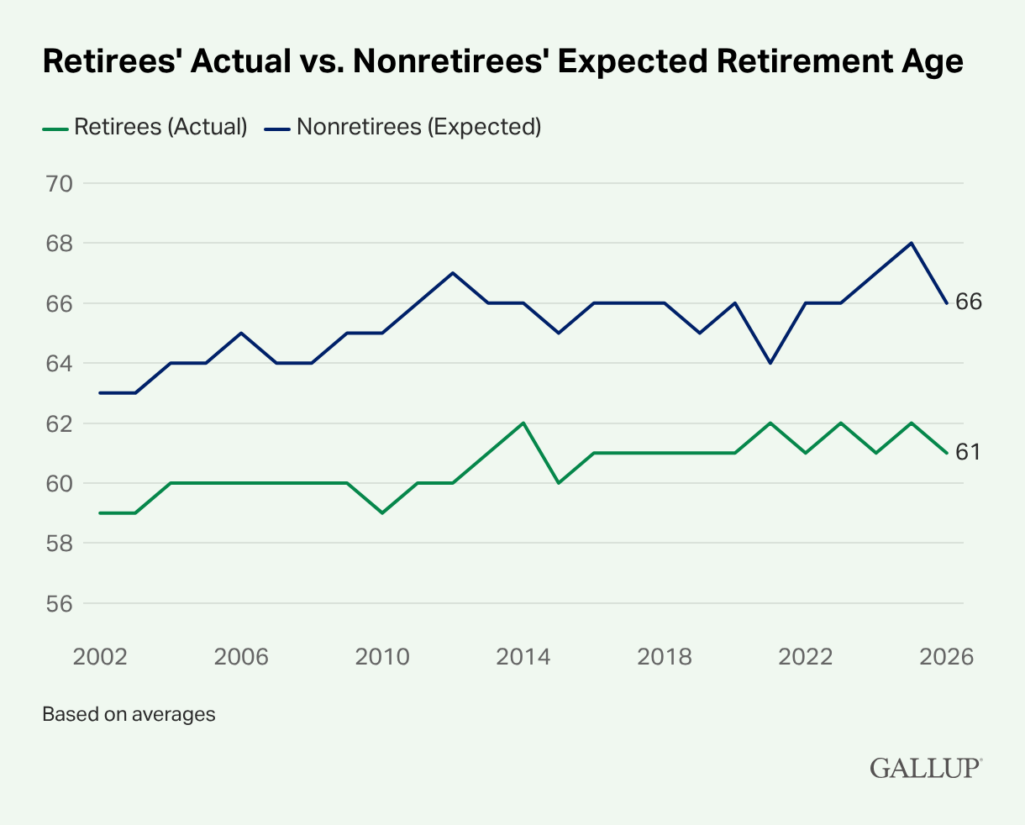

The common retirement age within the U.S. is 61. Most non-retirees anticipate to retire at 66. That five-year hole has held regular for 20 years, in response to Gallup’s April 2026 survey. About 46% of retirees left the workforce earlier than they deliberate, most frequently attributable to layoffs, well being issues, or caregiving calls for. The most typical Social Safety claiming ages are 62 and 66, primarily based on 2023 SSA knowledge.

If you happen to’re planning to retire at 66, that’s an inexpensive purpose. Most individuals set the identical goal. Most additionally find yourself retiring about 5 years sooner than they deliberate. Figuring out the place the typical retirement age lands is a key step towards a plan that holds up.

If you happen to’re desirous about retiring and questioning whether or not the timing is true, this information can assist you resolve.

The Common Retirement Age Is 61, Not the 66 Most Individuals Anticipate

Gallup has tracked this query for greater than 20 years. Its April 2026 survey places the precise common retirement age at 61. The precise determine has risen over that point, from 57 in 1991 to 61 at present. The goal most employees set, 66, hasn’t modified. That persistence suggests most Individuals are working into forces that push retirement sooner than deliberate, no matter intention.

These 5 years carry actual monetary weight. They lower into contributions whereas extending withdrawals, and so they typically arrive earlier than Medicare begins otherwise you’ve made your Social Safety choices.

Totally different knowledge sources put the typical retirement age anyplace from 61 to 65.5. None of them are fallacious. They only measure various things. Self-reported surveys, Social Safety claims knowledge, and labor drive participation evaluation every inform a special piece of the story.

The Most Widespread Age to Declare Social Safety Is 66, however 23% Nonetheless File at 62

In line with 2023 SSA claims knowledge analyzed by Bankrate, the most well-liked age to file for Social Safety is 66, adopted by 62. The weighted common age of newly retired employees submitting for advantages was 65.2 for each women and men in 2023, up from about 64 in 1998.

Right here’s how the 2023 claiming ages break down:

| Age | Share of latest claimants | Avg. month-to-month profit |

| 62 | 23.2% | $1,292.60 |

| 63 | 6.4% | $1,498.23 |

| 64 | 6.9% | $1,657.09 |

| 65 | 11.3% | $1,916.33 |

| 66 | 34.1% | $2,106.15 |

| 67 | 4.2% | $2,487.84 |

| 68 | 2.4% | $2,750.48 |

| 69 | 2.1% | $2,923.64 |

| 70–74 | 9.1% | $3,162.09 |

Supply: 2023 knowledge from SSA Annual Statistical Complement, 2024, by way of Bankrate

Social Safety’s full retirement age is now 67 for anybody born in 1960 or later. That’s the place your advantages attain their full quantity. Retiring at or earlier than 62 doesn’t require claiming early. You may delay advantages as much as age 70 even for those who’ve already stopped working.

39% of Employees Anticipate to Retire at 70 or Later, however Most Received’t

Gallup’s April 2026 knowledge reveals that the precise common retirement age has risen from 57 in 1991 to 61, however the goal employees set hasn’t moved.

The most recent analysis on this from the Transamerica Heart for Retirement Research’ twenty fifth Annual Retirement Survey finds:

- 39% of employees anticipate to retire at 70 or older, or don’t plan to retire in any respect (23% anticipate 70+; 16% haven’t any retirement plans)

- 10% anticipate to retire between ages 66 and 69

- 21% anticipate to retire at 65

- 29% anticipate to retire earlier than 65

Why Do Most Individuals Retire Earlier Than They Deliberate?

Most retirements arrive forward of schedule. In line with EBRI’s 2026 Retirement Confidence Survey, 46% of retirees left the workforce sooner than deliberate. In 76% of these circumstances, circumstances exterior their management drove the choice: a well being downside, a layoff, or a member of the family who wanted care.

Figuring out that doesn’t must be discouraging. Your plan simply must account for it.

Guardian Life’s 2025 evaluation discovered the pandemic briefly reversed a two-decade pattern towards later exits. By Q3 2021, 50.3% of U.S. adults 55 and older reported being out of the labor drive attributable to retirement.

If you happen to’re compelled out of labor earlier than you deliberate to retire, listed below are 6 steps you possibly can take.

Fewer Than Half of Employees Now Anticipate to Work Full-Time Previous 62

The pandemic modified what employees anticipate. A Might 2024 NY Fed evaluation discovered the share of employees anticipating to work full-time previous 62 fell to a collection low of 45.8% in March 2024, down from a pre-pandemic common of 54.6%. That drop lower throughout age teams, training ranges, and earnings brackets, and was bigger for girls than for males.

The longer-term structural image factors the opposite approach. A 2023 Pew Analysis report discovered adults 65 and older are projected to make up 8.6% of the labor drive by 2032, up from 6.6% in 2022. Older adults will account for 57% of labor drive progress over the subsequent decade. Early retirement spiked throughout the pandemic. The long-term pattern is towards working later.

Why Do Common Retirement Age Statistics Fluctuate So A lot?

No single supply measures retirement age the identical approach. Gallup makes use of self-reported surveys. The SSA tracks when individuals declare advantages. The Heart for Retirement Analysis (CRR) at Boston Faculty measures when labor drive participation falls beneath 50%. Every technique offers a special quantity.

The CRR measure has a recognized limitation. It consists of individuals who by no means supposed to work, like full-time homemakers and folks with disabilities. That pushes the quantity youthful than it ought to be.

The Financial Coverage Institute argues a extra correct technique seems to be at when half of the non-disabled workforce has exited. By that measure, the typical retirement age is 65.5.

Retirement Age Varies by Extra Than 4 Years Throughout U.S. States

The common retirement age ranges from 61 in Alaska and West Virginia to effectively above 65 in Hawaii, Massachusetts, and South Dakota. The place you reside can have an effect on if you’re prone to retire.

Earliest retirement states (avg. age 61–62):

- Age 61: Alaska, West Virginia

- Age 62: New Mexico, Michigan, Louisiana, Kentucky, Arkansas, Oklahoma, Alabama

Center retirement states (avg. age 63–64):

- Age 63: Oregon, Maine, Delaware, Nevada, Arizona, North Carolina, Georgia, Indiana, South Carolina, Ohio, Missouri, Mississippi

- Age 64: California, New York, Washington, Florida, Wisconsin, Illinois, Idaho, Pennsylvania, Montana, Wyoming, Tennessee

Newest retirement states (avg. age 65+):

- Age 65: Connecticut, New Jersey, Maryland, Vermont, Rhode Island, Minnesota, Colorado, New Hampshire, Virginia, Utah, North Dakota, Iowa, Nebraska, Texas, Kansas

- Later than 65: Hawaii, Massachusetts, South Dakota

Job availability, earnings ranges, value of residing, and the calls for of native industries all form these variations. States with extra manufacturing and handbook labor are likely to see earlier exits.

The Share of Individuals Retiring in Their 50s Has Almost Halved Since 2000

Early retirement isn’t what it was. The share of Individuals retiring between 50 and 54 dropped from 9% to six% over 20 years. These retiring between 55 and 59 fell from 19% to 11%. The pandemic created a spike, however the structural pattern factors towards later exits.

Fewer adults of their 60s are retired now than a technology in the past. Between 2002 and 2007, 41% of U.S. adults ages 60 to 64 have been retired. Between 2016 and 2022, that fell to 32%.

The post-pandemic image is extra difficult. Employees report a lot decrease expectations of working full-time previous 62, however many who retired early have since returned to work. The NY Fed describes the shift as “persistent” and “broad-based throughout age, training, and earnings teams.”

Longer retirements are a part of what’s driving the complexity. Life expectancy at 65 has grown from 12.7 years for males and 14.7 years for girls in 1940 to roughly 17.5 and 20.2 years at present, in response to SSA historic life expectancy knowledge and CDC 2022 very important statistics.

A retirement that runs 20-plus years requires a special plan than one constructed round 12 years. If you happen to’re constructing a plan that accounts for an extended life, see our information on how a lot cash you want for those who stay to 100.

The U.S. Retirement Age Is Close to the Center of the World Vary

Individuals retire later than employees in China, Russia, and the Philippines, and sooner than these in Denmark, Iceland, and Finland.

| Nation | Statutory Retirement Age | Notes |

| China | 63 (males); 55–58 (ladies) | Raised from 60/50–55 efficient January 2025; phasing in via 2040 |

| Russia | 63 (males); 58 (ladies) | Rising to 65/60 by 2028; reformed from 60/55 beginning 2019 |

| Philippines | 60–65 | Non-compulsory retirement at 60; obligatory at 65; varies by sector |

| United States | 61–65.5 (varies by measure) | |

| Denmark | 67 | Rising to 68 in 2030 |

| Iceland | 67 | |

| Finland | 65 | Projected to achieve 68–69 by ~2060 by way of life-expectancy indexing |

Sources: OECD Pensions at a Look 2025; World Inhabitants Evaluation 2026

Most international locations have handed laws to boost retirement ages as life spans develop.

The right way to Construct a Plan That Holds Up If You Retire 5 Years Early

A plan that solely works at your goal date is half a plan. Modeling what occurs for those who retire at 61 as a substitute of 66 is the place planning turns into protecting.

5 years adjustments the mathematics in 4 particular methods, and every one compounds the others:

1. Fewer contributions, extra withdrawals. Retiring at 61 as a substitute of 66 means 5 fewer years of saving and 5 extra years of drawing down. On a $500,000 portfolio, that hole can signify tons of of hundreds of {dollars} in misplaced progress, relying in your contribution charge and market returns. The sooner the exit, the longer your cash has to final.

2. Social Safety timing turns into a lever, not a given. Retiring at 61 doesn’t imply claiming at 61. You may delay Social Safety as much as age 70 even for those who cease working. Annually you wait will increase your profit by roughly 6–8%. If you happen to can fund the hole from financial savings or part-time work, delaying advantages can considerably enhance lifetime earnings. Claiming early since you want the cash is completely different from claiming early as a result of it matches your plan.

3. Healthcare protection turns into your first downside to resolve. Medicare doesn’t begin till 65. If you happen to retire at 61, you’re overlaying 4 years by yourself: via a partner’s plan, COBRA, market insurance coverage, or different choices. Market premiums for a 62-year-old common over $800/month earlier than subsidies. That’s an actual price range line most early retirees underestimate.

4. Your withdrawal charge wants a wider margin. A 30-year retirement (retiring at 65, residing to 95) already checks the bounds of a protected withdrawal charge. A 35-year retirement (retiring at 61) pushes additional into unsure territory. Stress-testing your withdrawal charge at each timelines (and figuring out the place the plan breaks) is how you discover out whether or not it’s worthwhile to save extra, spend much less, or construct in additional versatile earnings sources.

When you’re able to mannequin the numbers, the Boldin Planner permits you to run each situations aspect by aspect — financial savings, spending, Social Safety timing, and earnings sources — so you possibly can see precisely the place every one lands and what levers you’ve gotten left to tug.

Ceaselessly Requested Questions

Essentially the most-cited common retirement age within the U.S. is 61, primarily based on Gallup’s self-reported survey knowledge. Different measures give larger numbers. The SSA’s 2023 weighted common for brand spanking new profit claimants is 65.2. Labor drive participation evaluation places it at 64 for males and 62 for girls. The quantity shifts relying on what’s being measured and who’s included.

Most Individuals who retire early don’t select to. About 60% are pushed out by circumstances exterior their management, like a well being downside, a layoff, or a caregiving demand. The area between anticipated (66) and precise (61) retirement age has held regular for 20 years, per Gallup’s April 2026 survey. That hole displays unplanned exits greater than monetary readiness.

The preferred age to say Social Safety advantages in 2023 was 66, chosen by 34.1% of latest claimants, adopted by 62 at 23.2%. Claiming at 62 reduces your month-to-month profit by as much as 30%. Ready till 70 maximizes it. The weighted common claiming age throughout all new retirees in 2023 was 65.2 for each women and men.

Retirement age varies by greater than 4 years throughout U.S. states. Alaska and West Virginia common 61, the earliest within the nation. Hawaii, Massachusetts, and South Dakota common effectively above 65. Native labor markets, value of residing, and business combine all contribute to the variations.

Early retirement has been declining for 20 years and spiked throughout the pandemic. The share retiring between 50 and 54 fell from 9% to six% between 2000 and 2024. These retiring between 55 and 59 dropped from 19% to 11%. The pandemic created a reversal. Lengthy-term, older adults will account for 57% of labor drive progress via 2032.

About 5 years separates what Individuals plan and what occurs. Non-retirees goal 66; most retire at 61. That distinction is pushed largely by unplanned exits. A plan that works for each your goal date and an earlier compelled exit is probably the most sensible strategy.